{kind=link}

The Third Gulf War is wreaking all sorts of havoc with fossil fuel prices, from diesel to jet fuel to gas. Even for all that, on the surface, the price of a barrel of oil seems to have landed short of nightmare scenarios: Brent crude is currently back under $100 per barrel. That’s still far higher than the price at the start of the year, around $60 per barrel, but it’s not panic-inducing. Even prices at gas stations, while still elevated, are easing down from their highs over the last few weeks. Crisis averted? Not quite: this seemingly good news may actually indicate a deeper issue that economists call “demand destruction.” If that’s where we are, it could get pretty grim.

Demand destruction doesn’t mean that the underlying situation is improving: it means that things are so bad that consumers and investors aren’t willing to just absorb higher prices. Instead, they will try to shift off of the product (in this case fossil fuels) altogether, or at least as much as they can. It can also cause governments to implement resource-cutting policies, which could be strict enough to force changes in consumer behavior. Or, those policies could stick around even after the original crisis is gone. The main point is that this not some short term reaction to prices, but a sustained change that reshapes the economy.

As Javier Blas over at Bloomberg puts it, there are a few layers of defense that keep prices low even as oil supplies suddenly get squeezed. First, companies can simply sell the vast reserves they already have. Second, Gulf states have been finding other ways to sell oil without going through the Strait of Hormuz, the center of the crisis. Third, many countries have sold oil from out of their strategic reserves. According to Blas, these have worked so far, but may be reaching the limit of what they can do. Reserves eventually give out. The fourth and last defense is what we may be coming into now: demand destruction.

Not your normal supply and demand shift

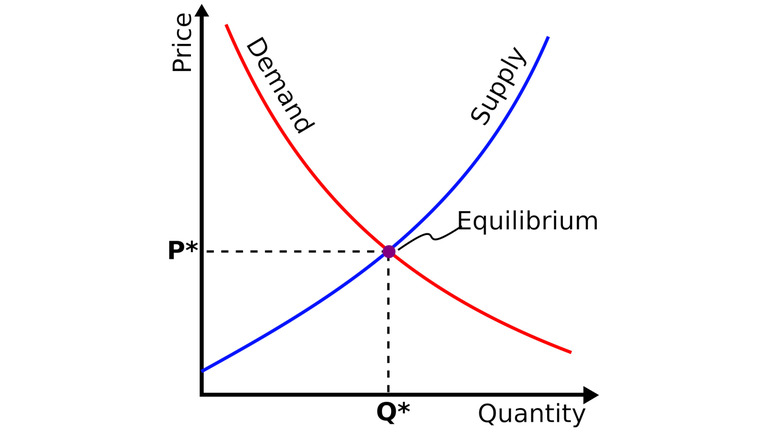

You might be wondering if this isn’t just the ordinary response to higher prices. Doesn’t demand always go down as prices go up? You may remember from Econ 101 that the price is just the point at which supply meets demand (as in the image above), so if the supply curve moves to the left (becomes constrained), the equilibrium price point rises and the quantity demanded goes down. This is normal market behavior. Those supply and demand curves will naturally fluctuate a little over time, but not far from the baseline.

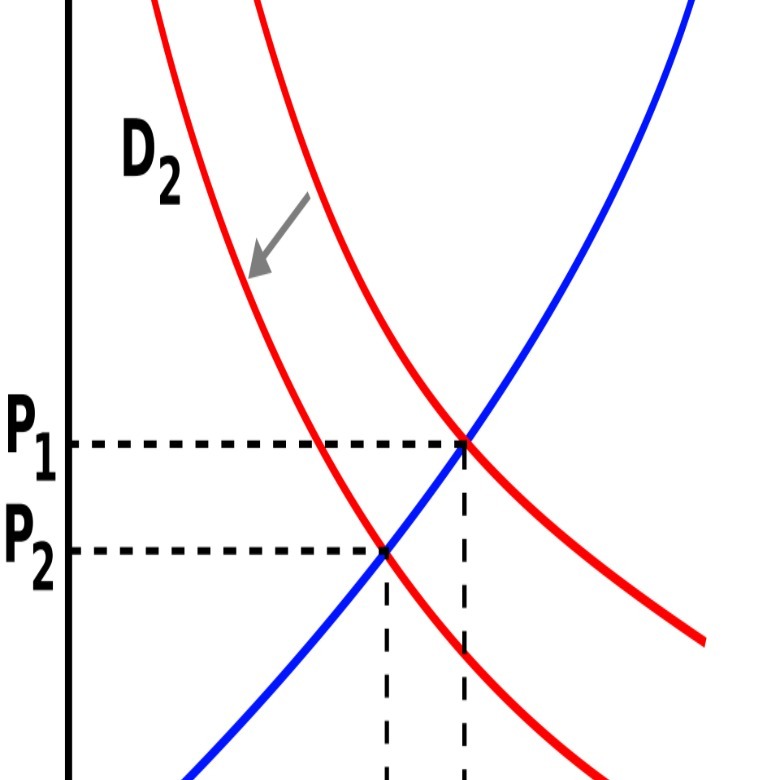

Demand destruction represents a more severe shift, however. It’s what happens when a supply crunch raises prices for so long, or by so much, that it forces structural, systemic changes. For the economic-minded among you, this is the equivalent of reducing not merely the quantity demanded, but the demand curve itself (as in the picture above). It is a permanent shift in market behavior, not just a temporary fluctuation. Thus, even if the supply goes back to normal, purchasing and pricing will never be the same again.

The International Energy Agency stated in a Tuesday report that we’re already here. In the Global South, factories and refineries are closing. Blas says that Pakistan, the Philippines, Vietnam, and Thailand are all starting to throw down restrictions on how much people can use resource-consuming goods, such as heating and air conditioning. Countries could start mandating work-from-home to eliminate commutes, or lowering speed limits. The longer this goes on, the more society habituates to it, and the harder it is to undo even if restrictions are later lifted.

And also, the more likely these restrictions spread to developed economies. Blas says:

If my math is right, the market needs to “destroy” demand by at least 8 million barrels a day or so. That’s more than the combined consumption of Germany, France, the UK, Italy and Spain.

What’s so bad about that?

The problem here is that oil is so central to how the modern economy functions that a massive change in overall demand has huge ripple consequences. If people drive less, they may buy fewer cars, or buy less frequently. That’s the entire auto industry at risk. Aviation could be in the same boat (that’s a metaphor that works and I’m sticking with it). Well, if people skip cars and planes, then the whole travel industry is at risk, and on and on it goes. Again, the threat isn’t that these industries could have a bad summer; the threat is that we’re looking at permanent changes to how people spend their time and money.

There’s a world where this could be a good thing. For example, people could substitute an ICE car purchase for an EV. That could potentially limit the damage to adjacent industries, like hospitality. And in good news for planet Earth, a widespread consumer shift away from fossil fuels could help fight climate change. If so, President Donald Trump, whose decision to bomb Iran began this crisis, could inadvertently become the greatest green energy champion in history.

Or it could go the other way. As NBC News reports, it’s possible that instead of substituting, consumers just reduce altogether: less driving, less flying, less cooking, less total economic activity. That is a classic recipe for a recession right there. This is why seemingly low gas prices might not be a great thing in this moment: they might indicate that stations are trying to entice people to drive as their behavior starts to change, before it changes forever.