{kind=link}

When a prospective buyer of a used vehicle from CarMax doesn’t qualify for financing, they’ll likely be offered a loan from Exeter Finance as a lender of last resort. Through its partnership with the country’s largest used car retailer, Exeter positioned itself at the pipeline of sub-prime borrowers, according to a ProPublica report. The lender would then use dubious extensions to stretch out loan periods and squeeze the poorest borrows for unbelievable sums of money.

Most Exeter loans are opened through CarMax, and ProPublica highlighted one sub-prime borrower to illustrate the economic situation of someone taking out this kind of loan. Jessica Patterson bought a $15,000 Kia Rio in 2017 from a CarMax outside of Kansas City, Kansas. She was a receptionist at a hearing aid sales center, making $12 an hour and had just moved out of a domestic violence shelter. ProPublica explains:

Like most subprime customers, her credit history was rife with unpaid bills. The debts were mostly from her ex-husband, she said.

The CarMax employee said she had good news, though: Exeter would lend Patterson the full amount needed to buy the Kia. Then the employee read the loan terms aloud. A six-year loan. A 25.17% interest rate. A monthly payment of $402.63. That would be a quarter of Patterson’s take-home pay, almost twice what consumer finance experts recommend.

She asked whether there were cheaper offers. None of the other companies were willing to give Patterson a loan, said the employee, who turned her computer monitor so Patterson could see. “Exeter was the only one there,” she said. According to rating agency reports, CarMax is the single largest source of Exeter’s business — responsible for some 50,000 loans per year.

Patterson agreed to the terms. To get to work and get her kids to school, she needed a car. Turning down the loan felt like giving up.

The loan’s staggering interest rate meant that Patterson would pay over $14,000 in interest to leave with the Rio, but she had no other option. She was aware of this because the amount was printed on the loan due to the Truth in Lending Act, but again, she had no other option.

Patterson quickly fell behind and requested two loan extensions by January 2018 as she took her family to free church dinners and visited food banks to save money to make payments. At first glance, Exeter might seem generous in offering relief but the change heaps even more debt onto borrowers through added interest. The report adds:

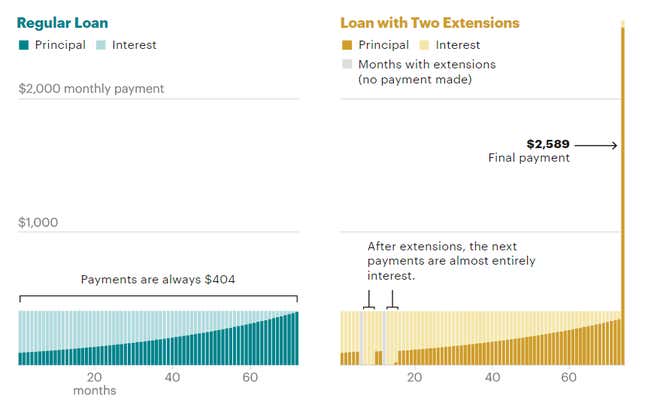

The company would simply move the December and January payments to the end of her five-year payment schedule, the representative told her, adding two months to the loan’s term. “It was instant relief,” Patterson said.

The extension seemed to be a courtesy from Exeter in a time of need. In fact, the company’s disclosures at the time stated “Extension fee: $0.00.”

The pause in payments, however, was anything but free. What Patterson didn’t know, and what she said Exeter didn’t tell her, was that every penny of her next five payments would go to the interest that built up during the reprieve. That meant she didn’t pay down the original loan balance at all during that time.

While the extension allowed her to keep her car, it added about $2,000 in new interest charges, which the lender did not clearly disclose.

Exeter eventually repossessed the Kia Rio from Patterson in 2021 after collecting $17,097 over three years while she was over $11,000 in debt. The lender then auctioned off the Kia for $13,800. So many more stories took the same course as Jessica Patterson’s. More than 200,000 Exeter loans are at least three payments behind schedule, and a quarter of these loans typically end with repayment stopping early.

You can read ProPublica’s full report here to learn more about Exeter’s highly questionable practices and the struggles of other borrowers.